Table of Contents

- Introduction

- What is Voluntary Repossession?

- Voluntary Repossession with No Late Payments

- Benefits of Voluntary Repossession

- Potential Consequences of Voluntary Repossession

- How to Initiate Voluntary Repossession

- Alternatives to Voluntary Repossession

- Impact on Credit Score

- Legal and Financial Considerations

- Conclusion

Introduction

Voluntary repossession with no late payments is a topic that has gained significant attention in recent years, especially among individuals facing financial challenges. While repossession is often associated with missed payments and financial mismanagement, voluntary repossession offers a unique option for borrowers who are unable to meet their loan obligations despite having a clean payment history. Understanding this process can help you make informed decisions and protect your financial future.

Voluntary repossession is a financial strategy that allows borrowers to return a financed asset, such as a car, to the lender without the lender having to take legal action. This option is particularly relevant for individuals who are facing financial hardship but have maintained a good payment record. By voluntarily surrendering the asset, borrowers can avoid the negative consequences of forced repossession while potentially minimizing damage to their credit score.

Read also:King Von Death The Tragic Loss Of A Rising Rap Star

In this article, we will explore the concept of voluntary repossession with no late payments in detail. We will discuss its benefits, potential consequences, and how it can be initiated. Additionally, we will provide insights into alternatives and the impact of this decision on your credit score. Whether you are considering this option or simply want to learn more, this article will equip you with the knowledge you need to make the best decision for your financial situation.

What is Voluntary Repossession?

Voluntary repossession refers to the process where a borrower voluntarily returns a financed asset, such as a vehicle, to the lender due to an inability to continue making payments. Unlike involuntary repossession, where the lender takes legal action to recover the asset, voluntary repossession is initiated by the borrower. This option is often considered when financial circumstances change, making it difficult to meet loan obligations.

Key features of voluntary repossession include:

- Proactive Approach: Borrowers take the initiative to return the asset, demonstrating responsibility and cooperation with the lender.

- Reduced Legal Hassle: By avoiding forced repossession, borrowers can prevent legal actions such as court filings or wage garnishments.

- Potential Cost Savings: Borrowers may save on repossession fees and other associated costs that typically arise during involuntary repossession.

Voluntary repossession is not a one-size-fits-all solution. It is essential to evaluate your financial situation carefully and consult with your lender to determine if this option is suitable for you. Understanding the terms and conditions of your loan agreement is crucial to ensuring a smooth process.

Voluntary Repossession with No Late Payments

One of the most common misconceptions about voluntary repossession is that it only applies to borrowers with a history of late or missed payments. However, voluntary repossession with no late payments is a viable option for individuals who have maintained a clean payment record but are facing unforeseen financial challenges. This scenario often arises due to sudden job loss, medical emergencies, or other unexpected expenses that strain the borrower's financial resources.

In such cases, voluntary repossession allows borrowers to:

Read also:Salt Trick For Men In Shower Enhance Your Shower Experience

- Protect Their Credit Score: By proactively addressing financial difficulties, borrowers can minimize the negative impact on their credit report.

- Avoid Legal Complications: Initiating the process voluntarily reduces the likelihood of legal disputes or aggressive collection efforts.

- Maintain a Positive Relationship with the Lender: Demonstrating responsibility and transparency can help preserve a good rapport with the lender, which may be beneficial for future financial transactions.

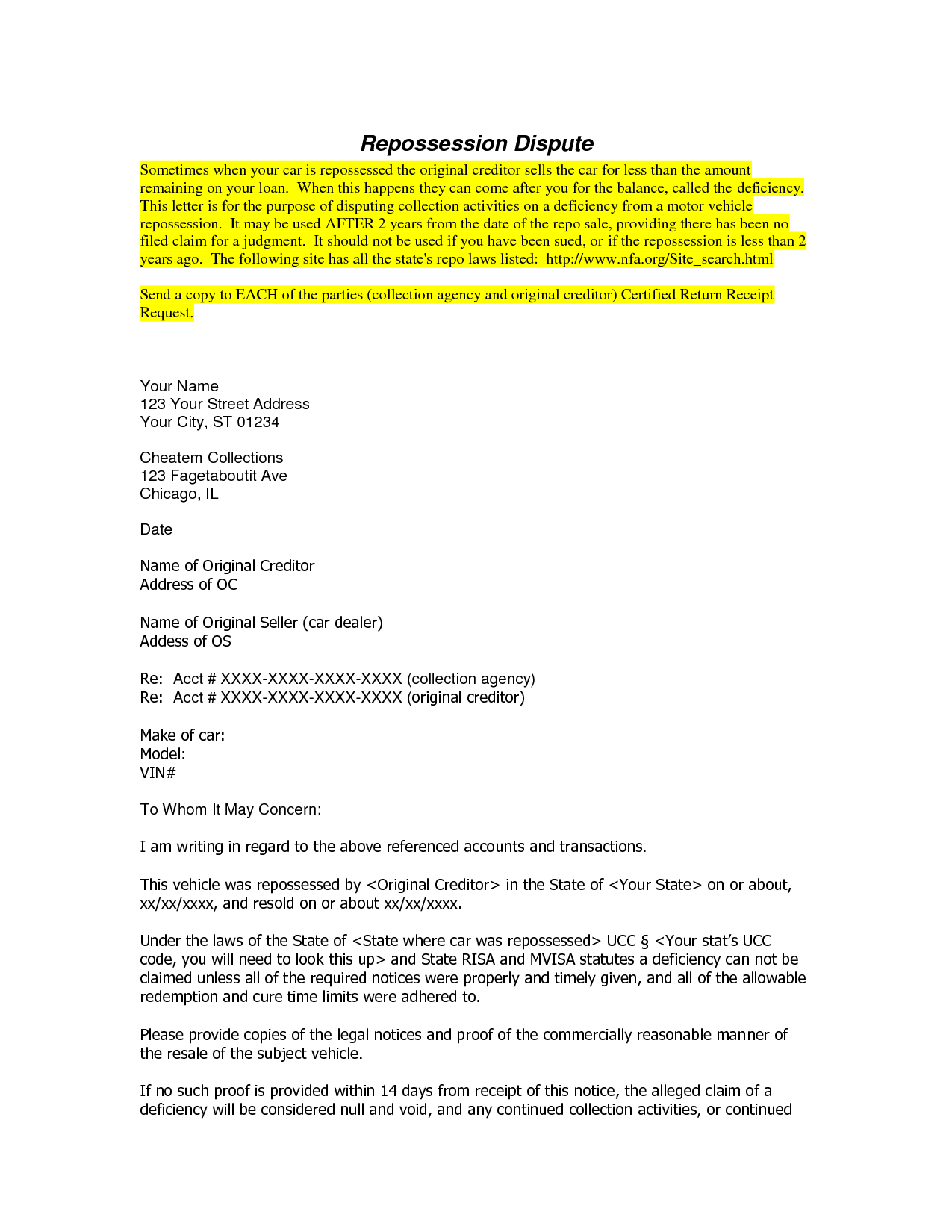

It is important to note that even with no late payments, voluntary repossession can still have financial implications. Borrowers may still be responsible for any remaining loan balance after the asset is sold, known as a deficiency balance. Understanding these potential outcomes is crucial to making an informed decision.

Benefits of Voluntary Repossession

Voluntary repossession offers several advantages, particularly for borrowers who are proactive in addressing their financial challenges. Below are some of the key benefits:

1. Avoiding Legal Action

By voluntarily returning the asset, borrowers can prevent the lender from initiating legal proceedings, such as filing a lawsuit or seeking a court order for repossession. This not only saves time and stress but also reduces the risk of additional legal fees.

2. Cost Savings

Involuntary repossession often involves significant costs, including repossession fees, storage fees, and legal expenses. Voluntary repossession allows borrowers to avoid these additional charges, potentially saving hundreds or even thousands of dollars.

3. Protecting Credit Score

While voluntary repossession will still impact your credit score, it is generally viewed more favorably than involuntary repossession. By taking the initiative, borrowers can demonstrate responsibility and mitigate the severity of the credit impact.

4. Maintaining a Good Relationship with the Lender

Initiating voluntary repossession shows that you are willing to cooperate with the lender and take responsibility for your financial situation. This can help preserve a positive relationship, which may be beneficial if you need to borrow money in the future.

While voluntary repossession offers these benefits, it is essential to weigh them against the potential consequences and explore all available alternatives before making a decision.

Potential Consequences of Voluntary Repossession

While voluntary repossession can offer several advantages, it is not without its drawbacks. Understanding the potential consequences is crucial to making an informed decision. Below are some of the key factors to consider:

1. Impact on Credit Score

Even though voluntary repossession is less damaging than involuntary repossession, it will still have a negative impact on your credit score. A repossession entry on your credit report can remain for up to seven years, making it challenging to secure new loans or credit cards during that period.

2. Deficiency Balance

After the asset is repossessed, the lender will typically sell it to recover the outstanding loan balance. If the sale proceeds are insufficient to cover the remaining balance, you may be responsible for paying the difference, known as a deficiency balance. This can create additional financial strain, especially if you are already facing hardship.

3. Loss of the Asset

Voluntary repossession means you will no longer have access to the financed asset. This can be particularly challenging if the asset, such as a car, is essential for your daily life or employment.

4. Emotional and Psychological Impact

Repossessing an asset, even voluntarily, can be emotionally taxing. It may lead to feelings of failure or regret, especially if you had maintained a good payment record prior to the decision.

Before proceeding with voluntary repossession, it is advisable to consult with a financial advisor or credit counselor to explore all available options and ensure you are making the best decision for your situation.

How to Initiate Voluntary Repossession

If you have decided that voluntary repossession is the best course of action, it is important to follow a structured process to ensure a smooth transition. Below are the steps you can take to initiate voluntary repossession:

1. Contact Your Lender

The first step is to reach out to your lender and inform them of your intention to surrender the asset. Be transparent about your financial situation and explain why you are unable to continue making payments. Many lenders are willing to work with borrowers who are proactive and cooperative.

2. Review Your Loan Agreement

Carefully review your loan agreement to understand the terms and conditions related to voluntary repossession. Pay attention to any clauses regarding deficiency balances, fees, or penalties.

3. Prepare the Asset for Return

Ensure that the asset is in good condition and ready for return. Remove any personal belongings and address any minor repairs or maintenance issues to avoid additional charges.

4. Schedule the Repossession

Work with your lender to schedule a convenient time and location for returning the asset. Some lenders may offer to pick up the asset, while others may require you to deliver it to a designated location.

5. Obtain Written Confirmation

Request written confirmation from the lender once the asset has been returned. This documentation can serve as proof that the repossession was voluntary and may be useful for addressing any disputes in the future.

By following these steps, you can ensure a transparent and organized process that minimizes potential complications.

Alternatives to Voluntary Repossession

Before proceeding with voluntary repossession, it is worth exploring alternative solutions that may help you avoid losing the asset. Below are some options to consider:

1. Loan Modification

Many lenders offer loan modification programs that can help borrowers facing financial hardship. These programs may include options such as extending the loan term, reducing the interest rate, or temporarily lowering monthly payments.

2. Refinancing

Refinancing your loan with a new lender can provide relief by securing a lower interest rate or more favorable terms. This option is particularly effective if your credit score has improved since you initially obtained the loan.

3. Deferment or Forbearance

Some lenders offer deferment or forbearance programs that allow borrowers to temporarily pause or reduce their payments. This can provide short-term relief while you work to improve your financial situation.

4. Selling the Asset

If you are unable to continue making payments, consider selling the asset yourself. This allows you to take control of the process and potentially pay off the loan balance without involving the lender.

5. Financial Counseling

Consulting with a certified credit counselor can provide valuable insights and guidance. They can help you create a budget, negotiate with lenders, and explore other options to address your financial challenges.

Exploring these alternatives can help you avoid the negative consequences of repossession while preserving your financial stability.

Impact on Credit Score

One of the most significant concerns for borrowers considering voluntary repossession is its impact on their credit score. While voluntary repossession is less damaging than involuntary repossession, it will still have a negative effect on your credit report. Below are some key points to understand:

1. Duration of the Impact

A voluntary repossession entry can remain on your credit report for up to seven years. During this period, it may affect your ability to secure new loans, credit cards, or even rental agreements.

2. Severity of the Impact

The extent to which voluntary repossession affects your credit score depends on various factors, including your overall credit history and the number of negative entries on your report. Borrowers with a strong credit history may experience a smaller impact compared to those with existing credit issues.

3. Steps to Mitigate the Impact

To minimize the long-term effects of voluntary repossession, consider taking the following steps:

- Pay Off the Deficiency Balance: If you are responsible for a deficiency balance, prioritize paying it off to prevent further negative entries on your credit report.

- Monitor Your Credit Report: Regularly review your credit report to ensure accuracy and address any errors promptly.

- Rebuild Your Credit: Focus on rebuilding your credit by making timely payments on other accounts and maintaining a low credit utilization ratio.

While voluntary repossession will have a negative impact, taking proactive steps can help you recover and rebuild your financial health over time.